By Marcus Moore

This article was originally published in the author’s personal Substack on June 1, 2026.

It’s late May 2026, and you’re a thirty-something Alaskan. Maybe you’ve got kids in Mat-Su schools, a job that actually depends on real energy costs staying sane, a deep love for this state that’s never stopped believing we can develop our resources without selling our kids’ future to the highest corporate bidder.

You’re scrolling through your favorite social media or the news after a long day, and all these fake and uninformed Americans hammering the same drum again.

Urgent. Thirty days. Closing window.

Generational opportunity. Pass the bill or lose the pipeline.

Arctic energy conference the Same stage, Same energy conference where, just one year earlier, Glenfarne’s own developer stood up and told the room the project looked economically attractive without any government handouts.

This year? Same stage, different tune not financeable without the tax abatement. And oh, by the way, they’re still not telling us the total construction cost.

That’s not urgency.

That’s a pressure play.

And today, in a Senate Finance Committee hearing that your tax dollars paid for, the project’s own adviser dropped the mask on the public record.

I want to be clear about something before we go further. This isn’t a pipeline hit piece. I want this thing built. I want the construction jobs. I want North Slope gas flowing so our lights stay on and our homes stay warm without us begging for imports.

But right now, this deal is shaping up to be bad if we build it the wrong way and just as bad if we don’t build it at all.

The only path that actually works is the one where the people who own the gas us, the residents who live here capture the real value.

Anything less turns Alaska into a resource colony a piece of geography that Glenfarne, federal tax-credit chasers, and Asian buyers strip for profit while our schools close and our sovereignty quietly disappears.

Let’s walk through exactly what the public record shows. Every number. Every name. Every testimony detail. Because the Governor’s thirty-day clock is explicitly designed to stop us from asking the hard questions and those questions are the whole ballgame.

The “Closing Window” Nobody Will Name

Governor, before anyone votes on anything, let’s start with the most basic question on the table: what window, exactly, is closing?

You have called this special session urgent because of a closing LNG market window. So put it in writing. Identify the specific market condition or contract deadline that requires this tax structure to be enacted within thirty days.

And while you’re at it, confirm whether the December 31, 2027 IRS construction deadline for Section 45V Clean Hydrogen Production Tax Credits is a factor in the timeline your office and Glenfarne are actually working against.

Because here’s the thing.

One year ago at your own energy conference, Glenfarne said the project looked great with no tax breaks.

This year they reversed course entirely not financeable without them, and they still won’t disclose the full construction cost. That reversal happened on your stage.

It has never been explained. And now you’re telling the legislature telling us that it has to be done in thirty days or the window closes forever.

Which window? Name it.

If the real urgency is preserving two billion dollars a year in stacked federal tax credits rather than some LNG market window, that is a fundamentally different conversation.

And the public was never told about it.

What the Adviser Actually Said in the Room

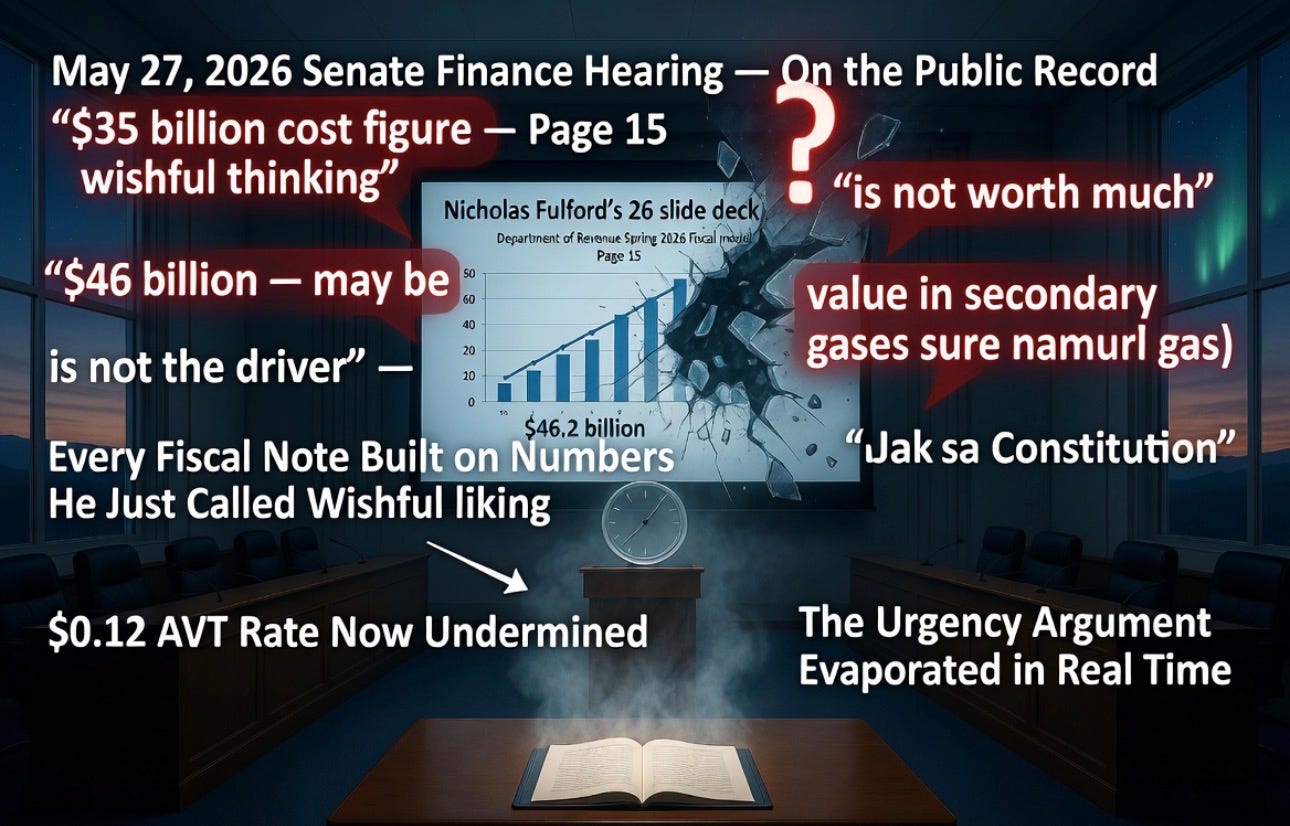

On May 27, 2026, GaffneyCline Senior Director Nicholas Fulford sat before the Senate Finance Committee as the project’s own expert adviser.

He was there to make the case for SB 2001.

What he actually did was blow up the fiscal foundation of the entire bill on the record, under questioning, in real time.

He called the $35 billion cost figure “wishful thinking.” On $46 billion he offered only a hesitant “may be.”

He said natural gas itself “is not the driver” of the project’s value and “is not worth much.”

When pressed on what actually is worth something, he pointed to “secondary gases.”

When a senator asked him to name them, he didn’t. NGLs, for what it’s worth, can’t even go in the pipe.

So here’s what that means in practice every single fiscal note attached to SB 2001 every number the Department of Revenue used to tell the legislature what this deal is worth to Alaska is built on the Spring 2026 DOR model using $46.2 billion as the construction cost assumption.

The exact number Fulford just called wishful thinking. On the public record. In the hearing room.

Mr. Fulford on what specific cost basis did GaffneyCline determine that the $0.12 per mcf Alternative Volumetric Tax rate in this bill is appropriate for Alaska?

The Worley cost update hasn’t been completed or disclosed to the committee.

So when, exactly, will that estimate be available for independent legislative review before a permanent tax structure gets locked in?

A senator in that room responded to all of this by saying the legislature may need to ask for a concession. But concessions get negotiated before you lock in permanent terms with fiscal stability provisions that prevent future legislatures from ever revisiting the deal.

Once SB 2001 passes, Alaska’s leverage on the tax rate is gone forever. The urgency argument the thirty-day clock evaporated in real time inside that hearing room.

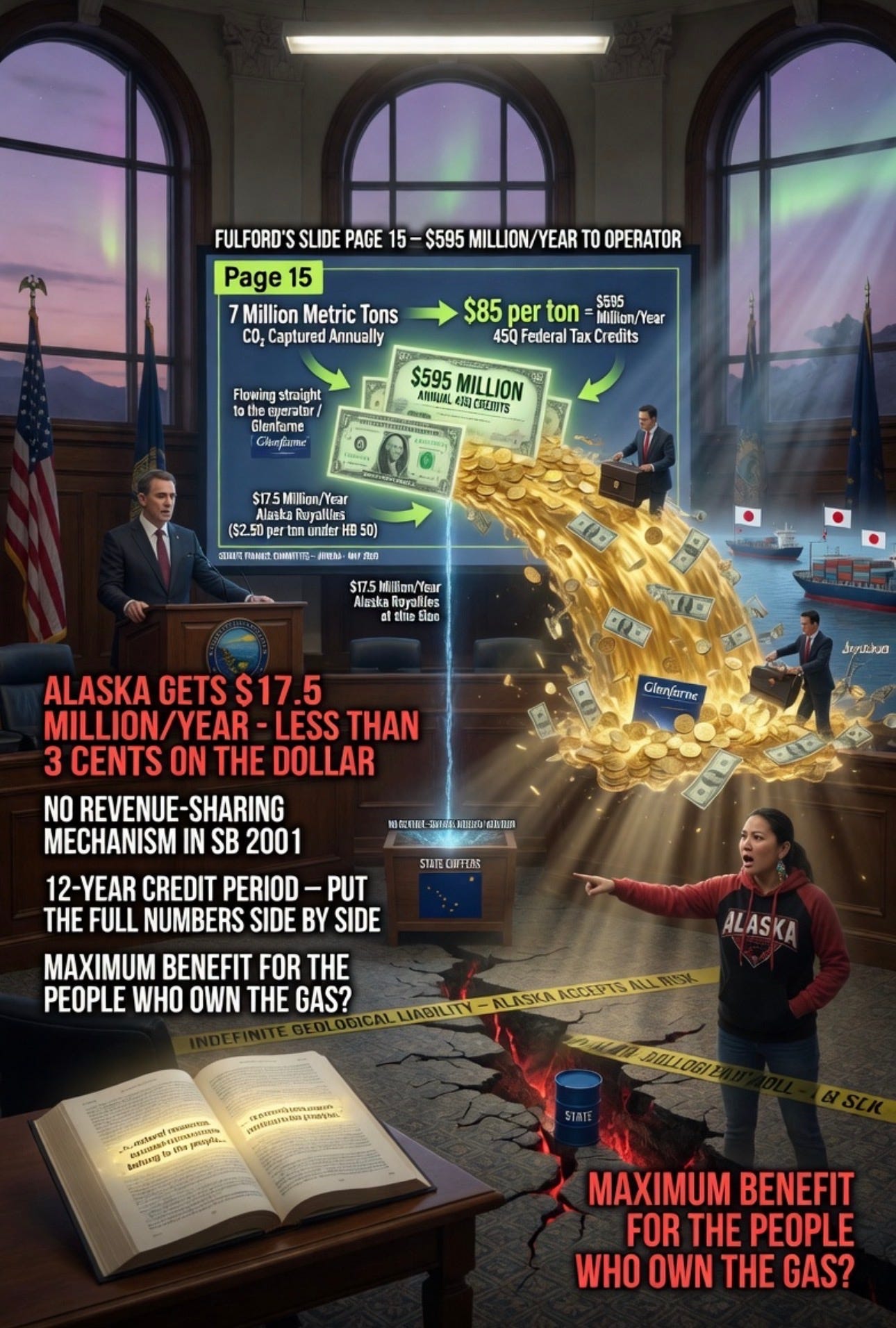

The $595 Million Carbon Capture Money Machine

Fulford’s own slides, Page 15, laid it out in clean numbers. Seven million metric tons of CO2 captured every year at the Gas Treatment Plant. Eighty-five dollars per ton under the federal 45Q carbon capture and sequestration tax credit. Run the math: that’s $595 million a year in federal tax credits flowing straight to the operator.

Now here’s what wasn’t in the slides.

Under HB 50, as amended by Senator Olson, Alaska collects $2.50 per ton in injection royalties on that same CO2 stream. Seven million tons.

Do the math again $17.5 million back to us. Less than three cents on the dollar for using Alaska’s geology, Alaska’s regulatory framework, and accepting Alaska’s long-term seismic liability underground. The 45Q credit runs twelve years once the facility is placed in service.

There is no revenue-sharing mechanism in SB 2001.

There is no statutory way for Alaska to touch any real slice of that $595 million annual windfall.

The state provides both the injection site and the legal framework, accepts the geological risk, and walks away with seventeen and a half million dollars while the operator banks nearly six hundred million.

What is the total projected 45Q credit value to Glenfarne and its partners over the full twelve-year credit period?

What is Alaska’s total projected royalty return over the same period?

Put those two numbers side by side. Put them on the record. Then explain to the people who own this gas why that ratio satisfies anyone’s definition of maximum benefit.

The Billion-Dollar Credit Nobody Mentioned

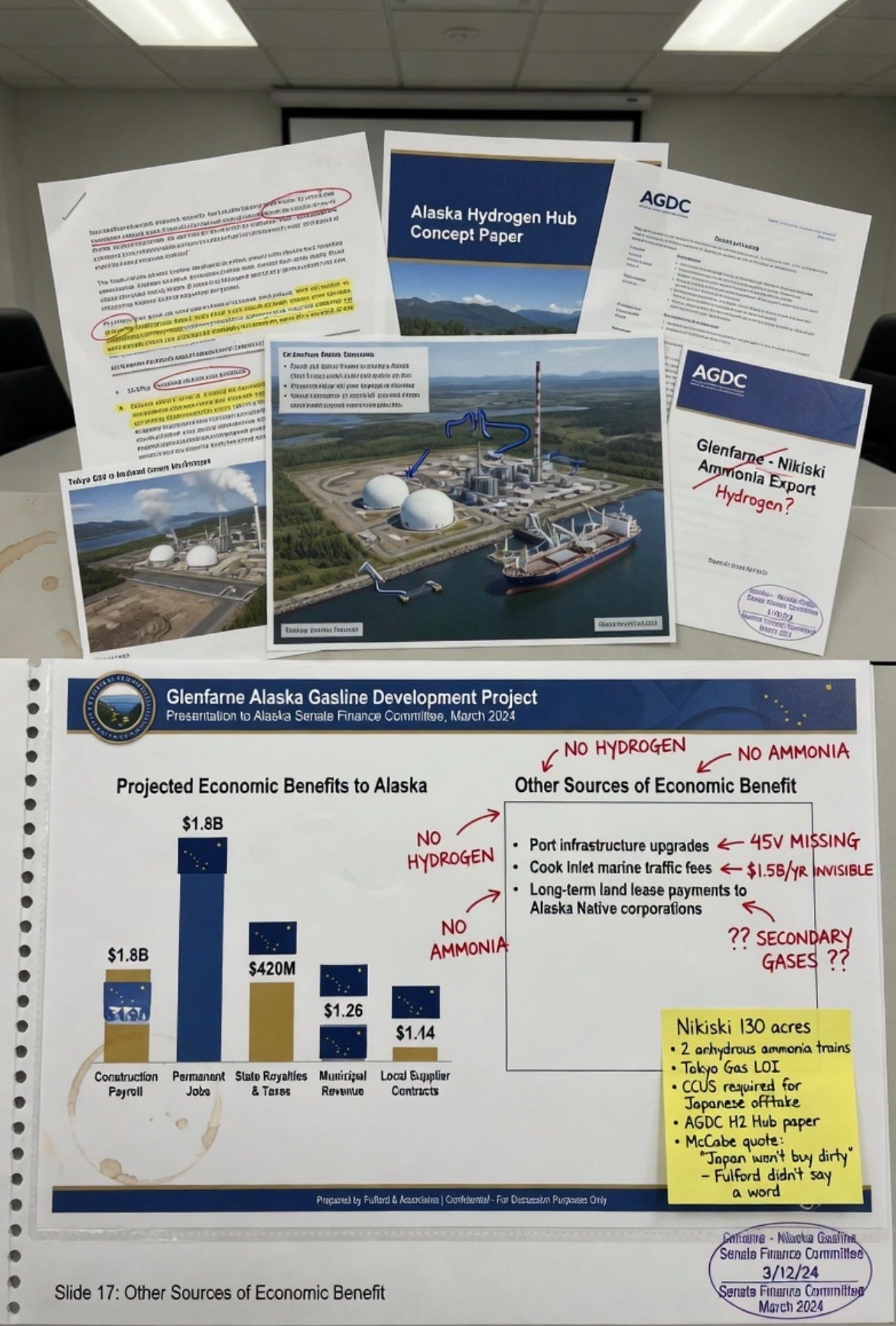

Now here’s where it gets wild. Because Fulford’s entire twenty-six-slide presentation didn’t mention hydrogen once.

Didn’t mention ammonia once. Didn’t mention Section 45V of the Internal Revenue Code at all, not in the section on economic benefits, not anywhere.

The Nikiski ammonia plant sitting on 130 acres with two anhydrous ammonia facilities and a cargo ship loading terminal? Invisible.

Completely absent from the “Other Sources of Economic Benefit” section of the project’s own adviser’s presentation to the Alaska Senate Finance Committee.

But the project record outside those slides tells the story clearly. Tokyo Gas letters of intent. Japanese institutional investors whose ESG rules demand carbon credentials. AGDC’s own hydrogen hub concept paper. Representative McCabe’s public statement that Japan won’t buy without CCUS.

That’s not environmentalism, that’s capital-market credentialing.

The Japanese buyers need a clean-energy label on the product to satisfy their institutional investors. The 45V credit is how you get it.

Here’s how the play works. At Nikiski, Steam Methane Reforming turns pipeline methane into hydrogen or ammonia for export. That process creates a separate CO2 stream. Capture it, inject it into Cook Inlet reservoirs, and the facility qualifies for up to $3.00 per kilogram of hydrogen under 45V. At 500,000 metric tons of hydrogen annually, that’s up to $1.5 billion a year in additional federal credits.

Those “secondary gases” Fulford wouldn’t name in the hearing room? That’s what he was talking about. The ones generating this second massive payout. The ones worth more than the gas itself.

Does Glenfarne’s project financial model include projected 45V credit revenue from hydrogen or ammonia production at Nikiski?

If so, what is the projected annual 45V credit value, and why was that figure not included in the section of the presentation titled “Other Sources of Economic Benefit”?

The question answers itself.

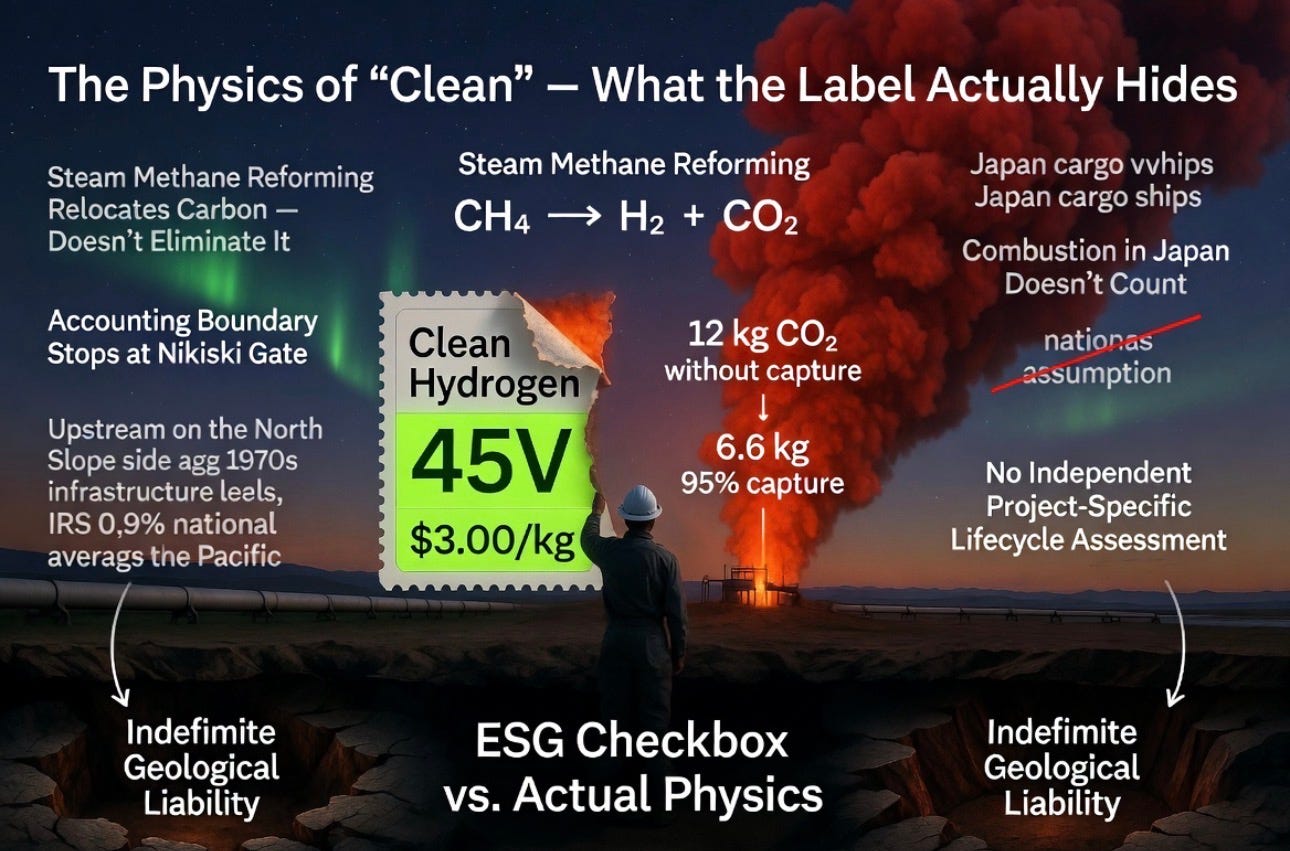

The Physics of “Clean” What the Label Actually Hides

Let’s talk about what the 45V “clean hydrogen” credential actually means, because this is where the whole environmental architecture of this deal gets shaky fast.

Steam Methane Reforming doesn’t eliminate carbon. It relocates it. The reaction splits methane into hydrogen and CO2. Without carbon capture, you’re looking at roughly twelve kilograms of CO2 per kilogram of hydrogen produced. Even at an optimistic ninety-five percent capture rate, about 6.6 kilograms remain.

And the capture equipment itself consumes fifteen to twenty-five percent of the facility’s gross output meaning you have to burn even more gas just to manage the CO2 the process creates.

To hit the full $3.00 per kilogram 45V credit tier, the IRA demands lifecycle emissions below 0.45 kilograms of CO2 per kilogram of hydrogen.

Here’s the problem, upstream methane leakage eighty times more potent as a greenhouse gas than CO2 over a twenty-year window from 1970s- and 1980s-era North Slope infrastructure isn’t audited project-specifically.

The model just uses a 0.9% national average. The accounting boundary stops at the Nikiski gate. Combustion in Japan doesn’t count. The ESG credential gets manufactured here. The emissions happen over there.

Net result across the full lifecycle wellhead to power plant is almost certainly more greenhouse gas than simply burning the natural gas straight. Alaska accepts indefinite geological liability in two seismically active basins in exchange for federal credit programs whose climate benefit has not been independently verified at full lifecycle scale.

At what emissions intensity does GaffneyCline project a Nikiski hydrogen facility would qualify?

What annual credit value per kilogram corresponds to that tier?

Has any independent lifecycle assessment been conducted using project-specific upstream methane leakage rates from North Slope production infrastructure, rather than the IRS default national average of 0.9%?

If the answer is no, then Alaska is accepting permanent underground geological risk in exchange for a clean-energy label that hasn’t been stress-tested against the actual physics of this specific project.

That’s not a climate benefit.

That’s a checkbox.

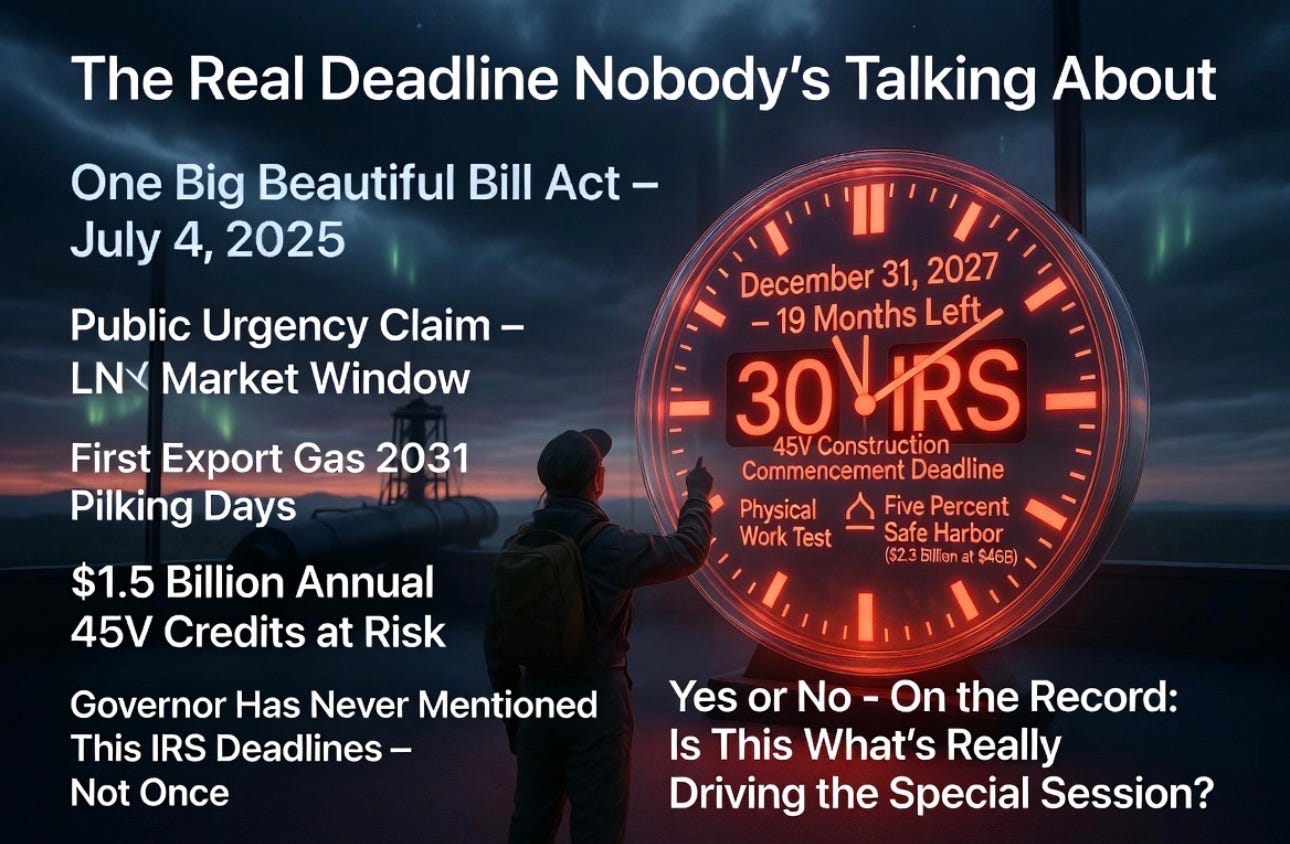

The Real Deadline Nobody’s Talking About

Here’s the thing that should make every Alaskan sit up straight and re-read the Governor’s public statements very carefully.

The One Big Beautiful Bill Act, signed July 4, 2025, moved the 45V construction commencement deadline to December 31, 2027.

That’s nineteen months from right now. To meet it, the project has to satisfy either the Physical Work Test or the Five Percent Safe Harbor which at $46 billion means committing $2.3 billion in verifiable construction expenditure. After that, there’s a four-year continuity safe harbor.

The project’s own timeline targets first export gas in 2031. Without SB 2001, without fiscal stability, without the legal framework locked in now, Glenfarne can’t credibly start construction in time to hit the IRS deadline. The 45V credit up to $1.5 billion a year disappears.

The Governor has never mentioned this IRS deadline in any public statement about the bill. Not once.

Has Glenfarne or any affiliated entity taken steps to establish beginning of construction for purposes of Section 45V?

Does Glenfarne’s project development timeline require SB 2001 to be enacted within this special session in order to preserve the ability to satisfy the IRS Physical Work Test or Five Percent Safe Harbor before December 31, 2027?

Yes or no. Both parts. On the record.

If the answer to that second question is yes, if the real reason for the thirty-day special session clock is preserving eligibility for a federal credit program worth up to $1.5 billion annually that the public has never been told about, then we have been misled about the nature of this urgency from the beginning.

We’ve been told this is about an LNG market window.

It may actually be about an IRS filing deadline.

Those are completely different things, and the people who own the gas deserve to know which one is driving the bus.

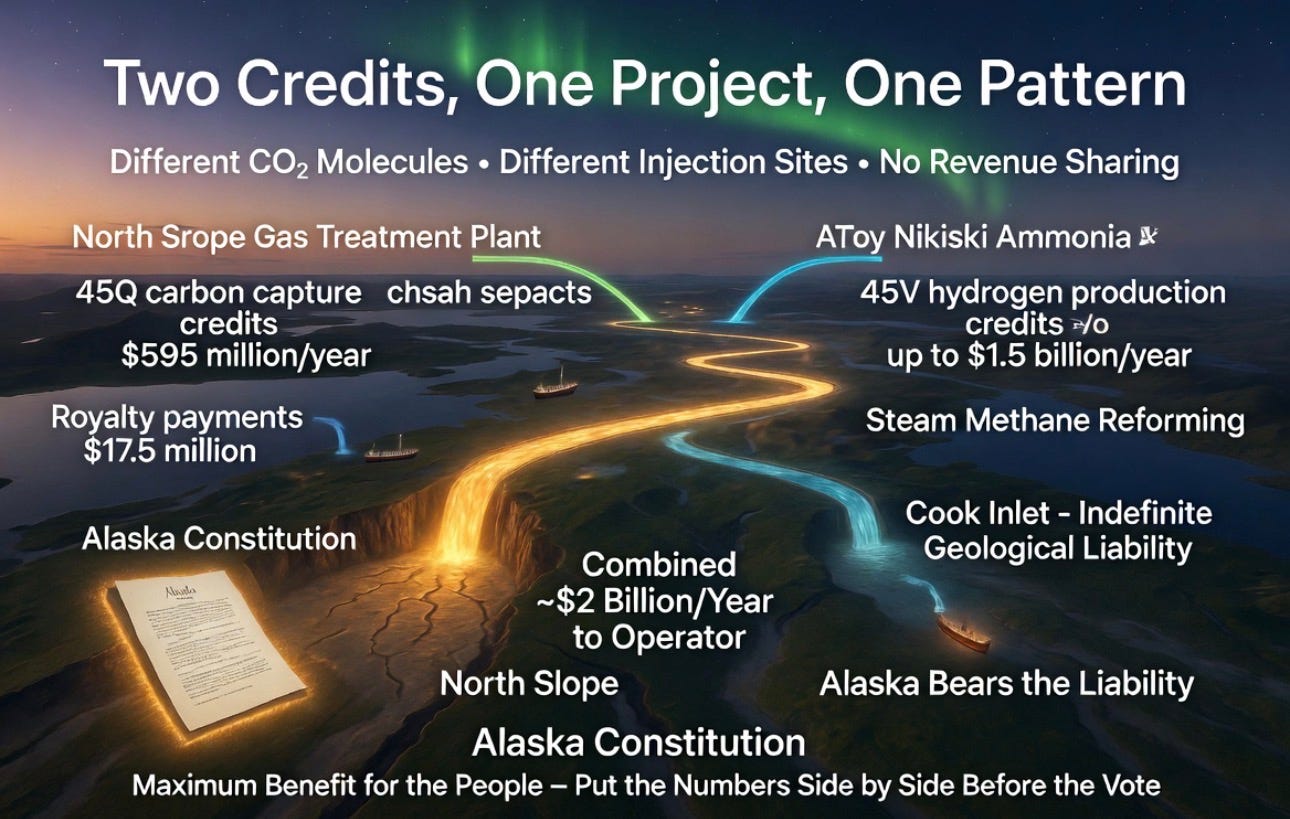

Two Credits, One Project, One Pattern

Let’s stack it up, because this is the picture that the Governor’s framing actively works to prevent you from seeing all at once.

45Q on the North Slope CO2 stream from the Gas Treatment Plant: $595 million a year, twelve-year credit period, Alaska gets $17.5 million in royalties on the same stream.

45V on the Nikiski CO2 stream from Steam Methane Reforming at the ammonia plant: up to $1.5 billion a year in additional federal credits, never mentioned in the adviser’s presentation, no revenue-sharing mechanism exists.

Different molecules. Different injection sites. Combined annual federal credit value approaching $2 billion paid by American taxpayers while Alaska provides both injection sites, accepts both long-term geological liabilities in seismically active basins, and rewrites its school funding formula to make it all possible.

Does Glenfarne’s integrated project financial model include projected revenue from both 45Q credits on the North Slope CO2 stream and 45V credits on a Nikiski hydrogen facility CO2 stream simultaneously?

What is the combined projected annual federal credit value to the operator across both programs at full project capacity?

What is the corresponding total Alaska revenue from royalties, AVT, and any other mechanism over the same period?

Put those numbers on the table.

Side by side. Public record. Before the vote. Because if the combined credit value to the operator approaches $2 billion annually and the total Alaska take is a fraction of that with no mechanism to share in the upside, the constitutional question isn’t academic. It’s the whole deal.

How the Special Session Killed the Better Deal

This is the third time the legislature has tried to move a tax package for this project.

The first two rounds HB 381 and SB 280 in the regular 34th Legislature were actually being shaped into something with teeth.

Senate Resources, under Chair Giessel, built a framework with a volumetric tax rate at the LNG plant of $0.25 per mcf. It included legislative approval requirements for major ownership changes. Investor disclosure. A $5 per mcf in-state gas price cap to protect Alaska utilities.

A ban on passing construction cost overruns to ratepayers.

SB 2001 drops the LNG plant rate to $0.12 per mcf. Less than half. Every single protective provision from the Senate Resources framework, gone.

The ownership change approval, the investor disclosure, the utility price caps, the overrun prohibition all of it stripped out in the special session version.

What specific analysis supports reducing the rate by more than half from the Senate Resources framework?

Which of the Senate Resources protective provisions will be restored as amendments before this bill passes?

Thirty days forecloses real committee work, forecloses public testimony, forecloses the kind of iterative process that produced those protections in the first place.

That compression wasn’t an accident. It was the design. You get a weaker deal with fewer safeguards when you can only run one lap around the track instead of three.

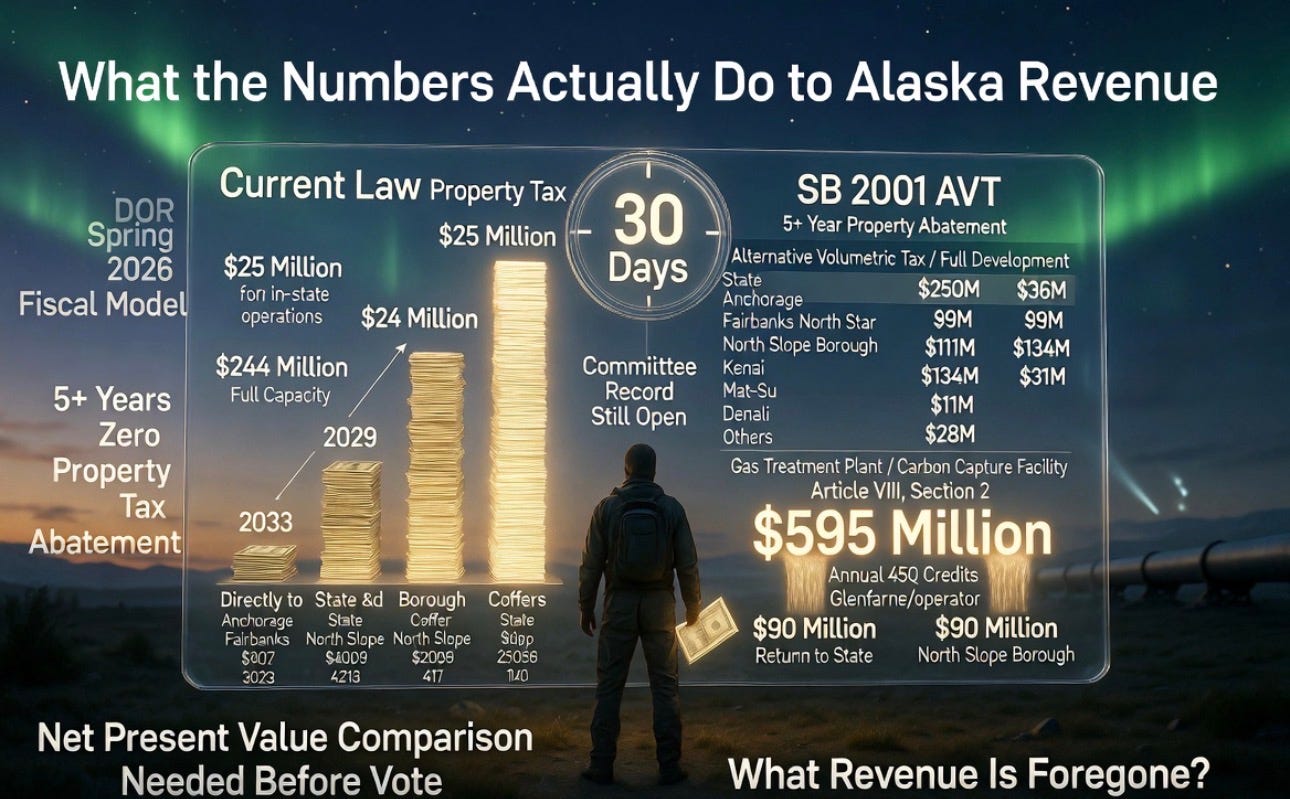

What the Numbers Actually Do to Alaska Revenue

The Department of Revenue’s Spring 2026 fiscal model projects that under current law, property tax revenue from this project would start at $25 million initially that’s 2029, when in-state operations begin and ramp to $244 million annually at full export capacity in 2033.

SB 2001 gives full property tax abatement during construction.

That’s five-plus years of zero. Then it switches to the Alternative Volumetric Tax, which DOR projects will return roughly a quarter of the 20-mill equivalent on infrastructure of this scale.

At full development the AVT breaks down like this: state gets $250 million, Anchorage $36 million, Fairbanks North Star $9 million, North Slope Borough $111 million, Kenai $134 million, Mat-Su $31 million, Denali $11 million, others $28 million.

The Gas Treatment Plant and carbon capture facility the engine of the $595 million annual 45Q credit return only $90 million combined to the state and North Slope Borough.

Read that ratio again.

Three federal credit dollars to the operator for every one dollar of combined state-plus-borough AVT from the facility generating those credits.

The operator’s annual take on that single facility exceeds Alaska’s combined take by roughly six to one.

What is the estimated total property tax revenue foregone during the abatement period?

What is the net present value comparison between current law property tax collections and the AVT structure over the full twelve-year 45Q credit period?

If the NPV of foregone property tax revenue during abatement plus the structural discount of the AVT rate compared to current law wipes out most of the apparent benefit of this deal, Alaskans need to see that math before the vote. Not after.

Rewriting the School Funding Formula While Schools Are Literally Closing

Sections 1 and 2 of SB 2001 permanently exclude AVT-subject project property from the taxable property base that determines how much corridor communities have to contribute to local school funding.

The largest infrastructure project in Alaska history will not count toward the school contribution formula. AVT revenue itself doesn’t count as a local contribution either.

Legislative Legal Services flagged this on April 27, 2026, in a memo to Senate Resources. Potential equal-protection problem under the Alaska Constitution.

Districts with pipeline infrastructure become differently situated from other districts. The memo recommended a full fiscal-impact analysis by school district before any vote. That analysis has not been presented to the committee.

Has DEED or Legislative Finance completed the comprehensive fiscal impact analysis by school district that Legislative Legal Services recommended? If not, why is this committee voting on a permanent restructuring of the school funding formula before that analysis is complete? What is the projected net change in state education funding obligation resulting from the formula restructuring, and which districts gain and which bear additional burden?

Because here’s what’s happening in those districts right now, while we’re having this conversation.

The Anchorage School Board voted in February 2026 to close three elementary schools: Fire Lake, Lake Otis, Campbell STEM. Ninety million dollar deficit. Fairbanks closed three schools. Juneau merged its two high schools into one campus. Ketchikan voted unanimously in April to close two more elementaries to close an eight million dollar gap.

Mat-Su the borough that literally hosts the natural gas pipeline corridor, the borough that stands to get $31 million in AVT revenue under this bill, faces a $23 million budget hole that school closures won’t even fully close.

Statewide, Alaska enrollment is at its lowest point since 1998.

This is the moment we’ve chosen to permanently restructure the school funding formula. Under a thirty-day clock. While the project’s own adviser is calling the cost assumption “wishful thinking” on the public record.

The kids in Mat-Su schools right now kids whose parents want the pipeline built and the jobs to materialize are going to school in a borough that’s closing classrooms while a legislative special session reshapes how their education funding gets calculated, based on construction cost numbers the developer’s own expert won’t fully stand behind.

That’s not a policy trade-off. That’s a moral failure in slow motion.

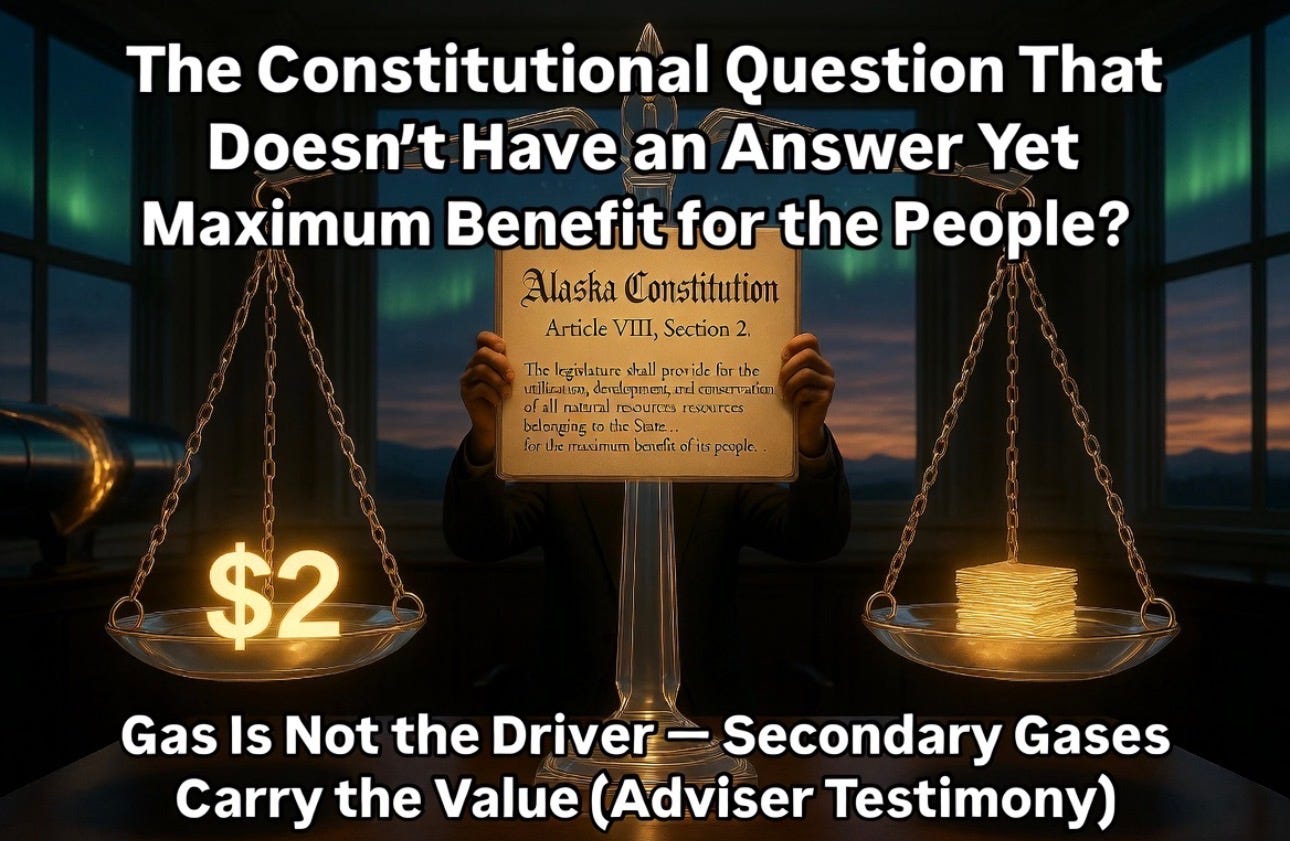

The Constitutional Question That Doesn’t Have an Answer Yet

Article VIII, Section 2 of the Alaska Constitution is not ambiguous:

“The legislature shall provide for the utilization, development, and conservation of all natural resources belonging to the State… for the maximum benefit of its people.”

GaffneyCline themselves put that provision on their March 18, 2026 Senate Resources presentation slide and compared it to other LNG-producing nations. They cited it as the governing standard. Then their adviser stood in front of the Senate Finance Committee and testified that natural gas “is not the driver” of the project’s value, that it “is not worth much,” and that unnamed secondary gases are where the value actually lives.

If the project’s primary economic engine is stacked federal tax credits under 45Q and 45V not LNG export revenue and if those credits are structured so that no meaningful revenue-sharing mechanism ties Alaska’s return to the operator’s credit receipts then the constitutional question isn’t a legal technicality.

It’s the central issue.

On what basis does the administration conclude that the AVT rates in SB 2001, which contain no revenue-sharing mechanism tied to federal credit receipts, satisfy the constitutional maximum benefit standard given that the project’s own adviser has testified that natural gas is not the economic driver and that secondary gases carry the primary value?

The words “maximum benefit” don’t mean “some benefit.” They don’t mean “the deal we could get in thirty days.”

They mean the best we can actually do for the people who own the resource.

And right now, the best deal on the table gives a private operator approaching $2 billion a year in federal credits with no mechanism for Alaska to share in that upside, while Alaska provides the geology, the regulatory framework, the seismic liability, and a rewritten school funding formula to make it all work.

That is not maximum benefit. That is resource colonialism with an Alaskan flag on it.

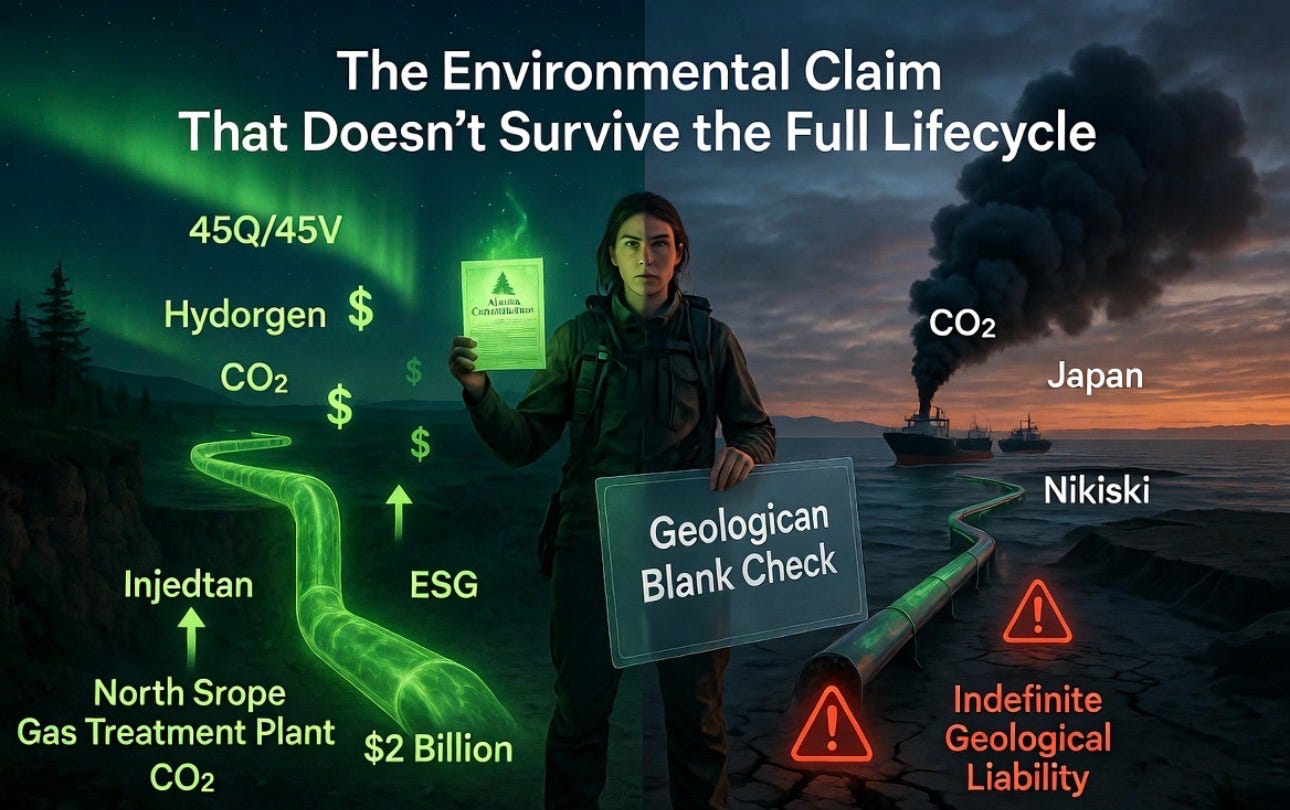

The Environmental Claim That Doesn’t Survive the Full Lifecycle

Both credit programs rest on environmental claims that collapse when you trace the full lifecycle.

The 45Q credit is justified as a climate benefit from carbon sequestration you’re re-injecting underground what the gas processing brought up. But the combustion CO2 from the methane that travels the fourteen-hundred miles of pipe to Nikiski and then gets shipped to Japan and burned? That’s outside the accounting boundary. It doesn’t count.

The 45V credit is justified as clean hydrogen production. But the accounting boundary stops at the Nikiski gate. The shipping emissions don’t count. The combustion at the destination power plant in Japan doesn’t count.

Net across the full wellhead-to-power-plant lifecycle accounting for upstream methane leakage from aging North Slope infrastructure, the energy cost of the capture equipment itself, and end-use combustion in Japan the greenhouse gas footprint of this project is almost certainly substantially worse than simply burning the natural gas directly.

Alaska accepts indefinite geological liability in two seismically active basins. The operator captures nearly $2 billion a year in federal clean-energy credits. The credits exist because Japanese institutional investors need an ESG label to satisfy their fund rules. The climate benefit, on a full lifecycle accounting, is largely fictional.

Has the administration commissioned or received any independent lifecycle emissions analysis of this project from North Slope wellhead through LNG or ammonia combustion at destination accounting for upstream methane leakage at project-specific rates and combustion emissions at the point of use?

If not, on what environmental basis does the state justify accepting permanent geological liability in two seismically active basins in exchange for federal credit programs whose climate benefit has not been independently verified at full lifecycle scale?

If the answer is no, then Alaska is writing a geological blank check for a program whose environmental rationale has never been stress-tested.

That’s not stewardship. That’s liability

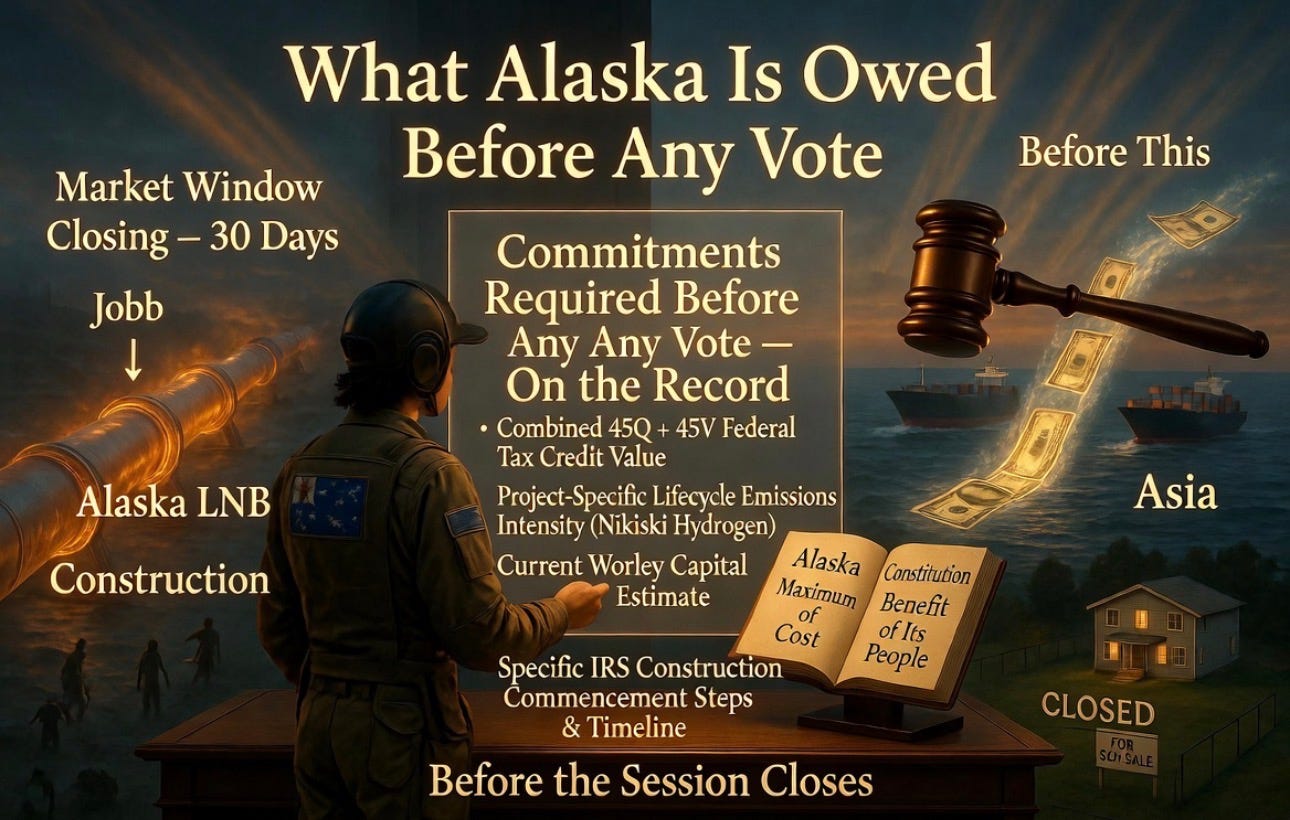

What Alaska Is Owed Before Any Vote

Before this committee votes before the session closes the public record needs four commitments made explicit.

Will the administration require Glenfarne to disclose, in writing, for the public record: the combined projected value of 45Q and 45V federal tax credits over the full credit period; the project-specific lifecycle emissions intensity of any planned hydrogen production at Nikiski; the current Worley capital cost estimate; and the specific IRS construction commencement steps Glenfarne plans to take and on what timeline, all of this before the permanent tax structure in this bill takes effect?

Yes or no. On the record.

Because right now, here’s what we know from the public record versus what we’ve been told.

We’ve been told there’s a market window closing in thirty days. The public record shows a potential IRS construction deadline for a $1.5 billion annual credit program that’s never been mentioned publicly.

We’ve been told $35 -$46-$78 billion is the project cost. The project’s own adviser called that wishful thinking.

We’ve been told the gas is the value. The project’s own adviser said gas isn’t the driver.

We’ve been told this is about LNG jobs and energy security. The economic architecture, as built, sends the primary upside stacked federal credits approaching $2 billion a year to the operator and foreign buyers while Alaska collects royalties worth less than three cents on the dollar and rewrites the school funding formula in the process.

The people who own the gas deserve better than this. Not “better” in the abstract better in the specific, documented, on-the-record way that the Alaska Constitution requires.

What You Can Actually Do Right Now

The committee record is still open.

Go to akleg.gov. Find your senator and representative. Every member has a public email address.

The questions in this piece every one of them are drawn directly from the public record, from Fulford’s testimony, from the DOR fiscal model, from the Legislative Legal Services memo, from the IRS statute.

They are not hostile.

They are not anti-development.

They are the bare minimum that any legislature working for the people who own the resources should have on the record before locking in permanent terms.

Copy them. Paste them into an email. Subject line: SB 2001 – Questions for the Record. Send it before the session ends. You don’t need to be a lawyer or an energy economist. You need to decide whether your legislators should have these answers before they vote.

Alaska First Means Getting This Right

We don’t have to choose between development and sovereignty. We never did.

Build it the wrong way…. With rushed tax breaks, no in-state supply commitments at fair prices, an AVT structure that captures a fraction of the value while the operator banks $2 billion a year in federal credits, equity dilution risks on our 25% stake, school funding formulas rewritten while classrooms empty — and we become the resource colony.

Jobs on paper. Sovereignty eroded. Ratepayers subsidizing Asia while future generations inherit the geological liability and the fiscal hole.

Don’t build it at all, and we miss the construction jobs, the revenue, the energy security, the domestic supply that keeps the lights on in the dark of January.

That failure is real too.

But the crossroads we’re standing at right now late May 2026, thirty-day clock, the project’s own adviser calling the cost number wishful thinking, the IRS 45V deadline ticking nineteen months away while nobody in the Governor’s office mentions it publicly, schools closing from Mat-Su to Ketchikan, this is exactly the moment where getting it right is still possible.

Not easy. Not inevitable. But possible.

The Constitution says maximum benefit for the people. Not maximum benefit for Glenfarne. Not maximum benefit for Tokyo Gas. Not maximum benefit for whoever ends up holding the 45V credits when the ammonia ships clear Cook Inlet.

Maximum benefit for the Alaskans who own the gas, who live on top of the geology, who send their kids to the schools that are closing while this deal gets rushed through a thirty-day session on assumptions the developer’s own guy won’t stand behind.

Alaska first doesn’t mean build anything at any cost. It means build it right, so the people who actually own this resource finally get the maximum benefit the Constitution has always promised them.

Every other version of this story is lose-lose. We’ve seen enough of those.

Let’s not write another one.

{kind=link}