By JOHN MORRIS

A broad coalition including physicians, chiropractors, physical therapists, podiatrists and more — representing the vast majority of healthcare providers in Alaska — recently brought suit to stop the repeal of the longstanding consumer protection known as the 80th Percentile Rule. As a member of that coalition, and a concerned Alaskan, let me explain to Must Read Alaska readers why:

After months of attempting to communicate in good faith with the Alaska Division of Insurance about the dangers of repealing the 80th Percentile Rule without a workable replacement, our coalition reluctantly took legal action to protect the countless Alaska families, workers and patients who will be impacted by this misguided repeal. If the repeal is allowed to stand, the elimination of this rule will severely jeopardize Alaskans’ ability to receive healthcare here at home, will return us to the days before the rule’s implementation in 2004 when Alaskans were saddled with surprise medical bills on top of their already high insurance premiums, and will result in little if any of the promised cost savings.

Every Alaskan, regardless of their politics or background, should care about this lawsuit because repeal of the 80th Percentile Rule all but guarantees an Alaska where it will be even harder to find a doctor, where wait times will dramatically increase, and where patients will have to pay even more out of their own pocket for healthcare.

Critics of the 80th Percentile Rule, led by Seattle-based insurance companies, have lobbied heavily to repeal this rule. Collectively, they’ve spent thousands of dollars spreading misleading messages such as Alaska’s doctors are getting paid too much, eliminating this rule is common sense and will lower healthcare costs, this is an outdated and unnecessary government regulation that raises costs and makes doctors more money.

But when you stop and review the facts there is so much more to this story. For example, if Alaska’s healthcare providers are being paid so much, why does Alaska face the most significant healthcare worker shortage of any state in the nation according to recent studies? One reason is that Alaska’s “competitive” salaries are no longer competitive; they’re being matched or surpassed by Lower 48 states hoping to recruit and retain medical professionals. But let’s use data, not anecdote.

According to Becker’s and Weatherby Healthcare, two reputable organizations that track physician compensation, Alaska doesn’t make the top 5 states for highest physician pay and, if you factor in the cost of living, we don’t even make the top 10. More than that, doctors in Alaska are getting paid less each year while insurance premiums have skyrocketed. That’s right, we are paying more each year for insurance but those same insurance companies are paying less each year per service. There are exceptions to this, but they are a small minority.

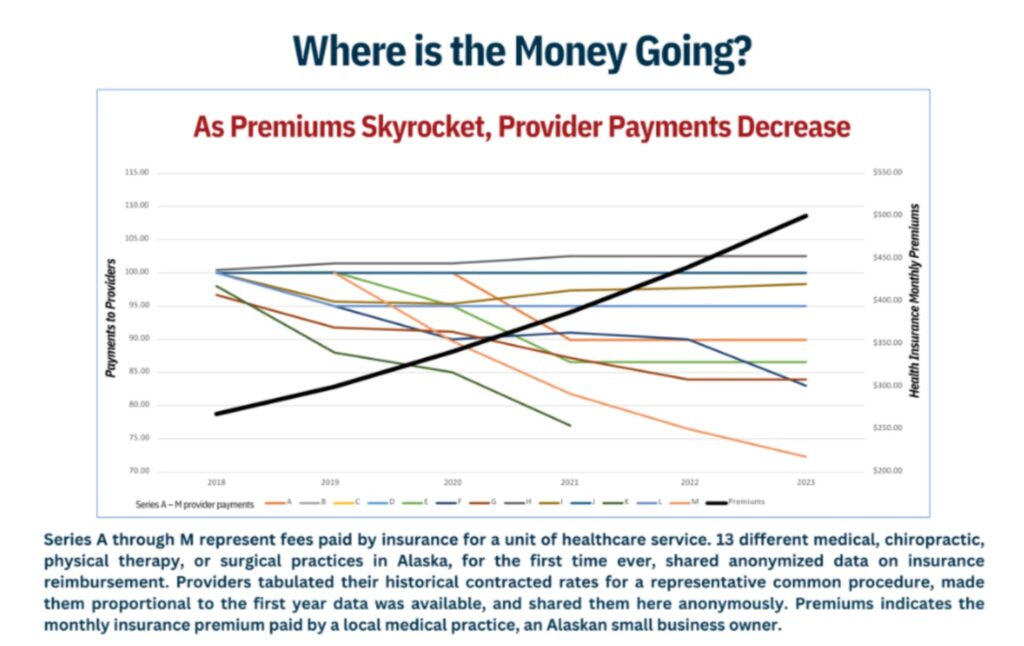

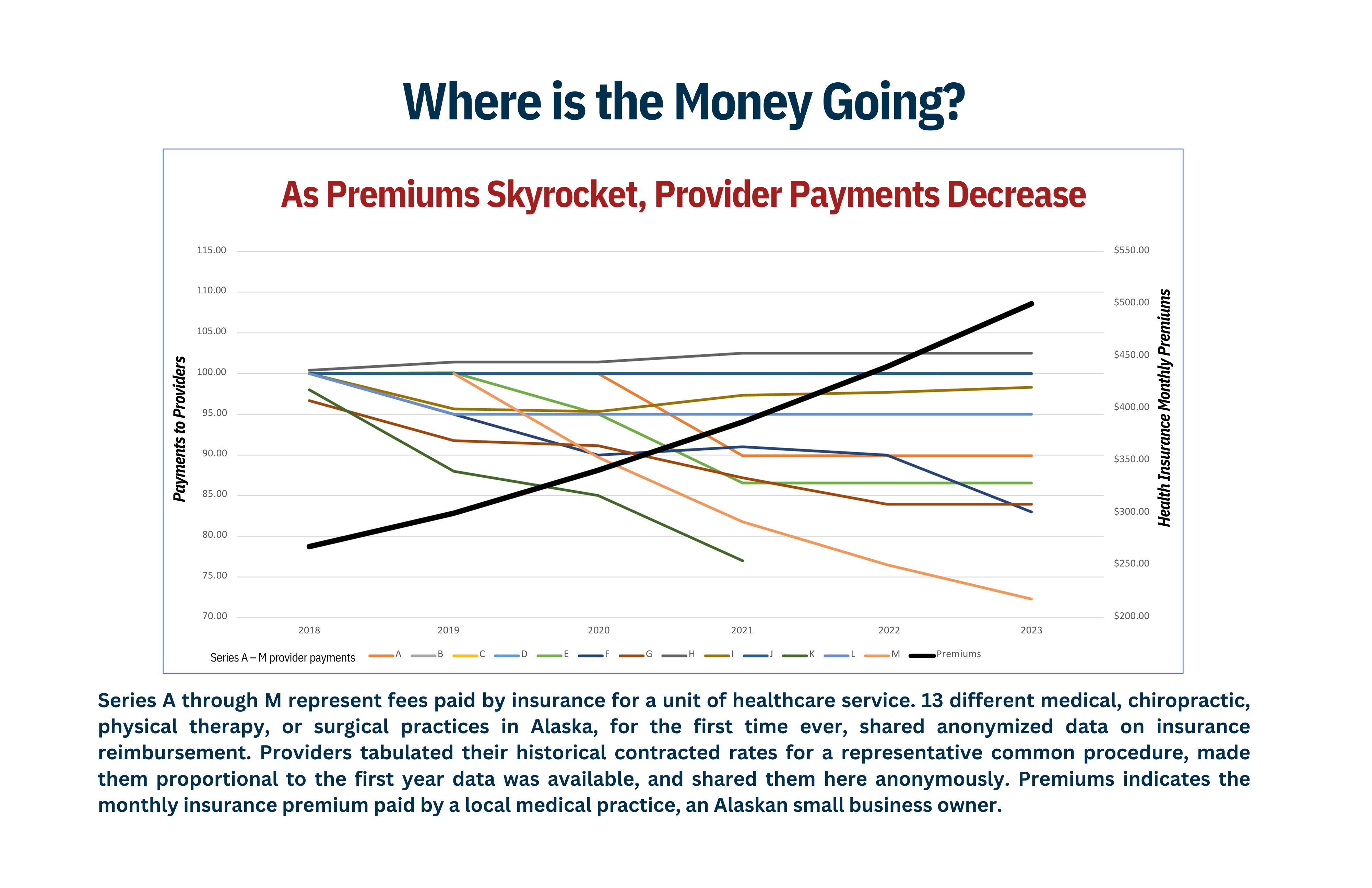

How do we know this? We did the work. We surveyed a broad spectrum of healthcare practices in Alaska and asked them to share how much insurance has paid them for a given service over the years. We then graphed those payment trends, together with how insurance premiums have risen, and got a striking picture. Again, despite each of us paying more in insurance every year insurers are, with few exceptions, paying less for the same care each year. Insurance pays less while premiums skyrocket.

If the Alaska Division of Insurance (DOI) knows that medical providers are receiving smaller reimbursements each year, why would they still push the repeal of the 80th Percentile Rule, which contains critical consumer protections and safeguards against insurance companies completely controlling the Alaska healthcare market?

We can’t speak for the DOI but the DOI’s Director, Lori Wing-Heier, told us that she based her decision making on data provided to her by an out of state company called FairHealth. FairHealth collects claims information and other data from insurers and then, for a fee, provides aggregated data on healthcare costs to various consumers across the country. Curious, we hired FairHealth too and paid them to give us the same data on how much insurance in Alaska has paid for a given service over the years – how much to deliver a baby or do a heart surgery, how much for a chiropractic treatment, and so on.

One of the first things we noticed about the FairHealth data was that it listed values for payments and charges for procedures that have never taken place – such as dozens of prices and payments for heart surgeries in Kodiak, Juneau, Fairbanks, and Ketchikan. In case you’re wondering, there are no heart surgeries in Kodiak, Juneau, Fairbanks, or Ketchikan. When we asked FairHealth about this they reported that they use mathematical methods to derive data when they don’t have any to report. In other words, they make it up. So we asked them for another spreadsheet of data, with only real (not derived) data in it. That spreadsheet was much, much smaller and wouldn’t have justified the DOI’s position.

The DOI and Premera say repealing this rule will result in lower health insurance costs – often citing an outdated and incomplete study that blames the 80th Percentile Rule for up to 24% of Alaska’s health care cost increases. But now that the rule has been repealed, we get a glimpse as to what the insurance companies and the Division of Insurance really think the 80th Percentile Rule is “worth”. The answer – not much. Despite the rule’s repeal insurance premiums are once again on the rise next year, just as they did last year, by about 17%, sometimes more. They are rising so much that they are making headlines. Premera now says the repeal of the 80th Percentile Rule will only amount to a savings of 2.5-4% (depending on who they speak to), despite previous claims that it would result in significant cost savings to policyholders.

While healthcare professionals and the 80th Percentile Rule are often blamed for the rising costs of healthcare in Alaska the real reasons for rising costs are sometimes simpler, if not a bit more inconvenient. Before each year starts insurance companies have to receive approval from the DOI for how much they can charge for premiums the following year. It’s called rate review. There are two insurers currently on the individual marketplace, Moda and Premera. Premera holds a virtual monopoly in Alaska but Moda is a big company too, doing over a billion dollars a year in revenue across all the states they operate in. For the year 2023, according to publicly available documents, Moda asked the DOI to only raise their prices 3.97%. It’s safe to assume that Moda would like to grow their business in Alaska, taking some customers from Premera, and having lower prices is a great way to do that. But that lower price request was not approved, and instead the DOI required Moda to raise their rates further by 12.1%. That’s 8% more than originally requested, hundreds of dollars per person more than what they asked for. In 2024 a similar story. Moda asked to raise prices 10.52% but instead was approved for 15.72%. For those interested, detailed information can be found at https://ratereview.healthcare.gov, including insight on what Premera’s prices have done in the same period.

In conclusion, despite insurance companies charging Alaskans more and providers being paid less for the same work, Alaska continues to grapple with massive shortages in healthcare workers. This shortage, which disproportionately affects vulnerable populations, such as seniors and veterans, continues to make receiving quality and timely medical care in Alaska a significant challenge. The Alaska DOI chose to use ‘derived’ data rather than real, locally sourced and timely data on insurance payments. The DOI decision-making has resulted in higher insurance costs by requiring Moda to charge more than their initial marketplace request – aligning their prices more closely with Premera’s rates. And lastly, all reforms and replacements proposed by the healthcare coalition to preserve the many consumer protections and safeguards found in the 80th Percentile Rule have been rejected by the DOI.

Repealing the 80th Percentile Rule without a replacement will turn back the clock on the significant progress Alaska has made in expanding our healthcare system over the last 20 years and will hand complete control over to out-of-state insurance companies. We encourage you to look beyond slogans and bumper stickers and think about whether you want your insurance company to choose who provides your healthcare, what it will cost you out of pocket if you disagree with their choice, and whether there will be a provider available for you to see at all. Please join us in working to make Alaska an even better, healthier place to live.

Five Reasons Repealing the 80th Percentile Rule Is Bad for Alaska:

- Fewer Consumer Protections: The 80th Percentile Rule provided Alaska patients with protections against predatory billing practices and surprise medical billing. Its repeal means fewer safeguards for policyholders, exposing them to greater risks without the safety net provided by the regulation. For example, recently several Providence based groups gave termination notices to Premera. With the 80th Percentile Rule these patients would be protected from big bills and could still see their regular doctor, no matter how the Providence and Premera fight plays out. Without it, they’re on their own.

- Shift in Power Away from Patients and Doctors: With the 80th Percentile Rule gone, access to reliable medical care in Alaska will be significantly impacted. That’s because the 80th Percentile Rule prevents insurance companies from completely controlling Alaska’s healthcare system. Without the 80th Percentile Rule, insurance companies have all the bargaining power, deciding which doctors you see, when and where you’ll see them, and arbitrarily deciding how much they’ll pay. Providers will be forced out-of-network by insurers who see no reason to contract with them and seek to narrow their networks.

- Premiums Are on the Rise: Despite, big out of state insurance companies insisting that the repeal of the 80th Percentile Rule would result in lower rates, premiums for Alaskans are set to skyrocket in 2024 –– with one insurer raising rates by 17.8%.

- Decreased Access Competition: Without Alaska’s 80th Percentile Rule, insurance companies have ZERO incentive to negotiate with your doctor. The result – they get to pick the winners and losers in our healthcare system; shrinking our healthcare market, reducing access, and driving specialists out of Alaska. For vulnerable populations like seniors, veterans, and rural residents, this would be catastrophic and would result in less access to care at home. Providers will be forced to limit or stop seeing non-privately insured payers all together as their fees will be drastically cut by insurers.

- Insurance Companies Continue to Reimburse Alaska Doctors Less, While Increasing Patient Premiums: Despite claiming doctors and medical providers are the primary driver of rising health insurance premiums, out-of-state insurance companies reimburse Alaska doctors less and less each year. How are local doctors the problem if 1) Alaska faces on the most significant healthcare worker shortage of any state in the nation and 2) insurance companies are paying providers less but charging you more?

For more information, please visit our website at www.reliablemedicalaccess.org.

John Morris is an Anchorage-based board-certified pediatric anesthesiologist and chair of the Coalition for Reliable Medical Access.

{kind=link}

{kind=link}