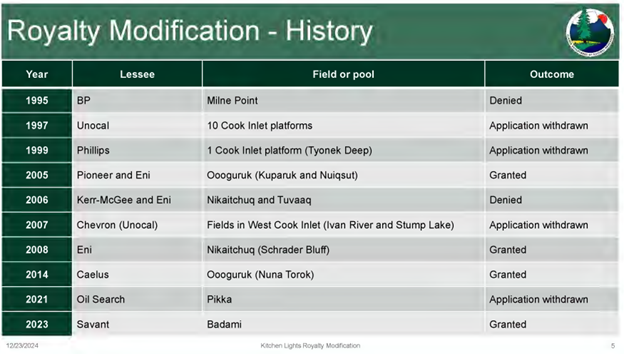

Cook Inlet remains the primary source of natural gas for Southcentral Alaska’s utilities, homes, and industry. Declining production in the mature basin has raised concerns about future shortfalls and reliance on more expensive imported liquefied natural gas. At the center of the discussion is the Kitchen Lights Unit (KLU) with a 25% royalty burden. The Alaska Department of Natural Resources (DNR) approved a targeted royalty modification in February 2025 after rigorous review, reducing the state’s 12.5% royalty to 3% on seven key leases until a cumulative gross revenue target is met.

HB 271, which advanced from the House Resources Committee in February 2026, seeks to codify that 3% rate legislatively starting January 1, 2026. The debate highlights tensions between administrative flexibility, legislative certainty, fiscal responsibility, and energy security. DNR’s data-driven findings emphasize that the modification extends field life, delivers additional gas volumes, and generates net revenue gains for the state—directly supporting efforts to address supply challenges.

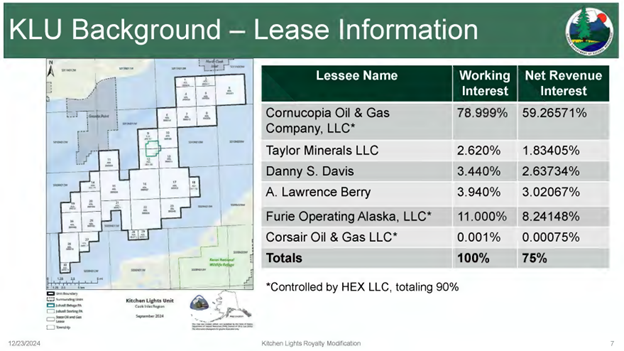

HEX/Furie’s story underscores local commitment amid industry consolidation. Furie Operating Alaska filed for Chapter 11 bankruptcy in August 2019 after operational setbacks, including and a 2018-2019 gathering line freeze and cost overruns. HEX Cook Inlet LLC (100 percent Alaskan-owned), submitted the winning bid at a court-supervised auction in December 2019. The acquisition of Furie, along with affiliated companies Cornucopia Oil & Gas Company and Corsair Oil & Gas, closed on June 30, 2020. Alaska Industrial Development and Export Authority (AIDEA) financing of up to $7.5 million, approved in March 2020, proved instrumental, enabling the purchase and development of the Beluga and Sterling formations plus associated infrastructure—a 15-mile subsea pipeline, onshore facility, and Julius R platform, now the Allegra Leigh. HEX/Furie presented the final loan payment to the AIDEA board 8 months early, receiving accolades for turning around the distressed Kitchen Lights Unit and returning the unit to stable gas production.

Since taking over, HEX/Furie invested in foundational fixes. As the only Alaskan-owned operator in Cook Inlet, HEX/Furie supplies gas exclusively to Southcentral utilities and the Marathon refinery in Nikiski. Its presence maintains competition alongside larger producers like Hilcorp, helping stabilize supply for a region that accounts for the majority of the state’s population. Without continued investment, the unit’s output—critical for residential heating, industrial use, and avoiding costlier alternatives—would face premature curtailment.

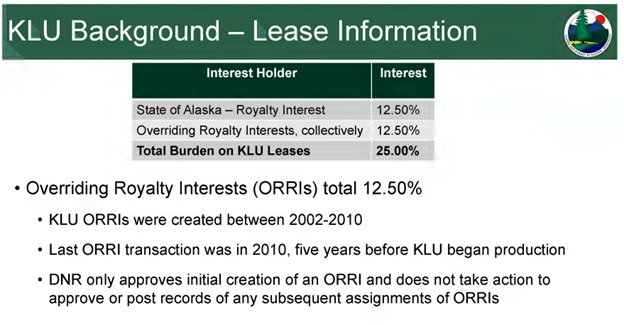

The royalty structure at KLU reflects decades of standard State of Alaska leasing practices layered with private contractual interests that the State of Alaska approved. All leases, issued between 2000 and 2007, carry the state’s standard 12.5% royalty as lessor. No modifications occurred until the 2025 determination. Overriding royalty interests (ORRIs) add another fixed 12.5% burden, carved exclusively from the working interest owners’ share and free of operating costs.

Prodigy Alaska LLC originated roughly 14% of the total ORRI burden (2002–2006). Pacific Energy Alaska Operating LLC contributed 13% in 2007. Escopeta Oil Co. LLC (later renamed Furie Operating Alaska in 2012) reserved the largest share, approximately 68% overall, including a 7% reservation to itself in 2010 on the Sterling and Beluga participating areas where current production occurs. In 2010, Escopeta and Taylor Minerals LLC returned a combined 5% burden on certain leases to equalize the total non-cost-bearing load at 25% across the unit.

The last ORRI transaction occurred in 2010—five years before sustained production began in November 2015. No new ORRIs have been created since, and the combined 25% burden remained unchanged through HEX’s 2020 acquisition. DNR approved the initial creation of these ORRIs between 2002 and 2010 with no other known restructuring of interest since the department does not track these assignments.

However, the outside Lower 48 owners tried one more attempt to structure the KLU for their benefit. In September 2011 Escopeta attempted to transfer an ORRI from Escopeta and the three minority Working Interest Owners, the result would have been to have the net revenue interest of 75%. Then DNR Division of Oil & Gas Director, Bill Barron, rejected this attempt to push additional costs onto the operator of the unit stating:

“…This ORRI share, combined with the state’s royalty interest, leaves the working interest owners with only 75% of the production revenue who must bear 100% of the costs of exploration and development… The impact of a high ORRI percentage on the economic potential of the leases will adversely affect the state’s interests… As 12.5% total ORRI would create a long-term, unfavorable encumbrance on these leases that could decrease the likelihood of the lease being develop. I therefore find that the transfer would adversely affect the state’s interests, and I therefore deny these applications”

In this instance DNR recognized the potential negative consequences of the old owners attempts to push costs away from themselves. But DNR still had allowed the creation of 12.5% of ORRIs along with the typical State 12.5% royalty share. This structure squeezes margins as production naturally declines and per-unit costs rise, particularly for a small independent operator funding all capital and operating expenses while paying both the state royalty and ORRIs out of its 75% working-interest share. Data presented to the legislature has shown that the KLU is unique in the total royalty that was forced to conduct business.

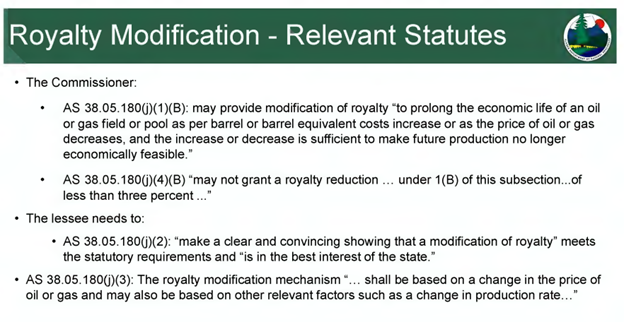

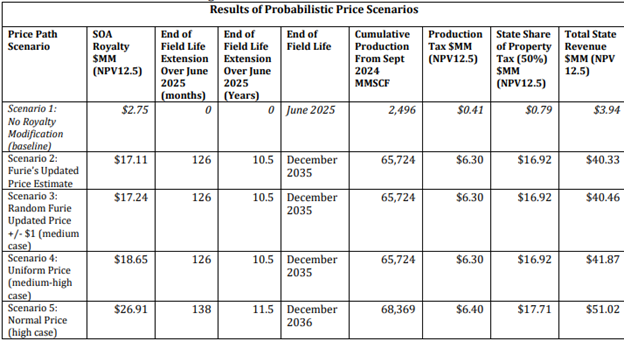

DNR’s Final Findings and Determination, issued February 3, 2025, provides the evidentiary foundation for relief. The application initially covered all 30 leases, but approval targeted seven leases reachable from the Allegra Leigh (Julius R) Platform for redevelopment. Cumulative production through October 2024 totaled 41.65 billion cubic feet (Bcf). Output peaked at 28,447 mcfd in November 2018 before declining to approximately 9,100 mcfd by October 2024 amid falling reservoir pressures. Without modification, DNR modeling projected shutdown by June 2025 after only 2.5 Bcf more production.

DNR conducted independent stochastic analysis across multiple price and production scenarios. The modification sets the state royalty at 3% monthly until cumulative gross revenue from September 1, 2024, reaches a DNR-adjusted $712 million target (based on full platform redevelopment costs for up to 12 new sidetracks/re-drills by 2028), after which it reverts to 12.5 percent. The change is retroactive to September 1, 2024, and non-assignable without approval, with six-month audits and termination rights if conditions change.

Projections show a 10.5-year average field-life extension to approximately December 2035. Additional production reaches 63.2 Bcf in likely scenarios. State revenues increase substantially: in the base case, net present value (NPV at 12.5 percent discount) rises from $3.94 million without relief to $40.33 million with modification—an incremental gain of $36.38 million from higher royalties ($14.36–$15.90 million), production taxes ($5.89–$6.30 million), and the state’s 50% share of property taxes ($16.13–$16.92 million). Even conservative models confirm net gains. DNR concluded with clear and convincing evidence that continued production would otherwise become uneconomic and that the modification serves the public interest by extending local supply, preserving jobs, and maximizing economic benefits compared with early shutdown.

HB 271, sponsored by Rep. Zach Fields (D-Anchorage), directly references DNR’s findings. It directs the commissioner to modify the leases to a 3% royalty rate beginning January 1, 2026, with legislative intent language emphasizing the unit’s importance for reliable energy, job protection, and reduced import reliance. The bill passed the House Resources Committee 7-2 on February 2026 after amendments failed. Public testimony revealed opposition. Jeff Landfield of the Alaska Landmine, representing himself, described the measure as a “political handout” to HEX, citing the operator’s bankruptcy purchase, prior property-tax disputes, and earlier unsuccessful bills. Additional letters of support were submitted by Alaskan companies – Fox Energy & Maritime Helicopters – emphasizing the benefits of having Alaskan companies developing Alaska’s resources.

Committee debate centered on process and certainty. Rep. Donna Mears (D-Anchorage) proposed a 2030 sunset and removal of intent language, favoring reliance on DNR’s administrative process and warning of legislative overreach. Supporters, including sponsor Fields, Rep. Dan Saddler (R-Eagle River), and Rep. Julie Coulombe (R-Anchorage), countered that the bill endorses—not overrides—DNR’s research. Saddler noted the pragmatic reality: “We’d rather have fifty percent of a loaf than one hundred percent of no loaf at all.” Fields stressed multi-year predictability for capital-intensive investments like jack-up rigs. A conceptual amendment refined language from “avoid” to “reduce” reliance on imports. The bill advanced, reflecting recognition that statutory backing complements DNR’s durable administrative contract.

Public testimony and legislative concerns focused on politics and precedent, yet they contrast sharply with DNR’s technical analysis. Critics portrayed relief as favoritism to one operator without acknowledging that the 12.5% ORRI burden originated entirely with prior working-interest owners years before HEX’s involvement.

DNR’s modeling demonstrates clear net benefits to the state treasury and public—more gas, more revenue, sustained jobs—rather than a zero-sum loss. The administrative process already included transparency, business input, and six-month audits; HB 271 simply adds legislative durability across administrations to support financing.

DNR’s approach accelerates addressing Cook Inlet’s gas shortage. Without relief, KLU production would have ended mid-2025, removing a key competitor and forcing utilities toward costlier imports or reduced supply. The modification and proposed statutory codification enable platform redevelopment, delivering an additional 63.2 Bcf over a decade-plus extension. This bolsters Southcentral supply, potentially moderating prices through increased competition and local production. Utilities have indicated the added volume could lower ratepayer costs in the near term while providing breathing room for broader basin strategies.

A recurring question in the debate concerns the ORRI holders: given that the state and HEX/Furie accept reduced returns to sustain operations, why have ORRI owners not voluntarily reduced or sold portions of their 12.5% burden? ORRIs are perpetual, non-operating contractual interests created through development transactions and approved by DNR at origination. The 2010 equalization to a uniform 25% total burden reflects prior owners’ business decisions. Prior to submitting its application, Furie reported to the Department that it made multiple efforts to work with the current ORRI owners to either reduce their burden or sell their interest to Furie to prolong the life of KLU. These attempts in 2023 and in 2024 were unsuccessful.

Ultimately, DNR’s Final Findings and Determination offer an evidence-based roadmap. By confirming uneconomic conditions without relief and quantifying substantial incremental benefits, the analysis prioritizes sustained production and supply stability from an Alaskan-owned and operated gas producer. HB 271 builds on that foundation by providing the statutory predictability needed for major investment.

As Cook Inlet matures, pragmatic tools like targeted royalty adjustments help maintain local energy security, preserve Alaskan jobs, and generate net public revenue. The KLU case illustrates how data-driven administration, combined with legislative support, can bridge the gap between declining legacy fields and future needs without compromising the state’s long-term interests.

{kind=link}